In a global context that has generally continued to perform positively, the Spanish economy is still undergoing intense and differential economic growth regarding the euro area.

The mutual feedback between economic growth and job creation -although the growth rate of the latter has stagnated in the first four months of the year- continues to support consumption and disposable income. Moreover, the opening of our economy outwards enables the export sector to play an increasingly prominent role, with significant capacity to compete on international markets. In this scenario, we maintain our December forecast for the Spanish economy of a 2.8% and 2.4% GDP increase in 2018 and 2019, respectively. We foresee that GDP growth will continue to be based both on the positive performance of internal and external demand.

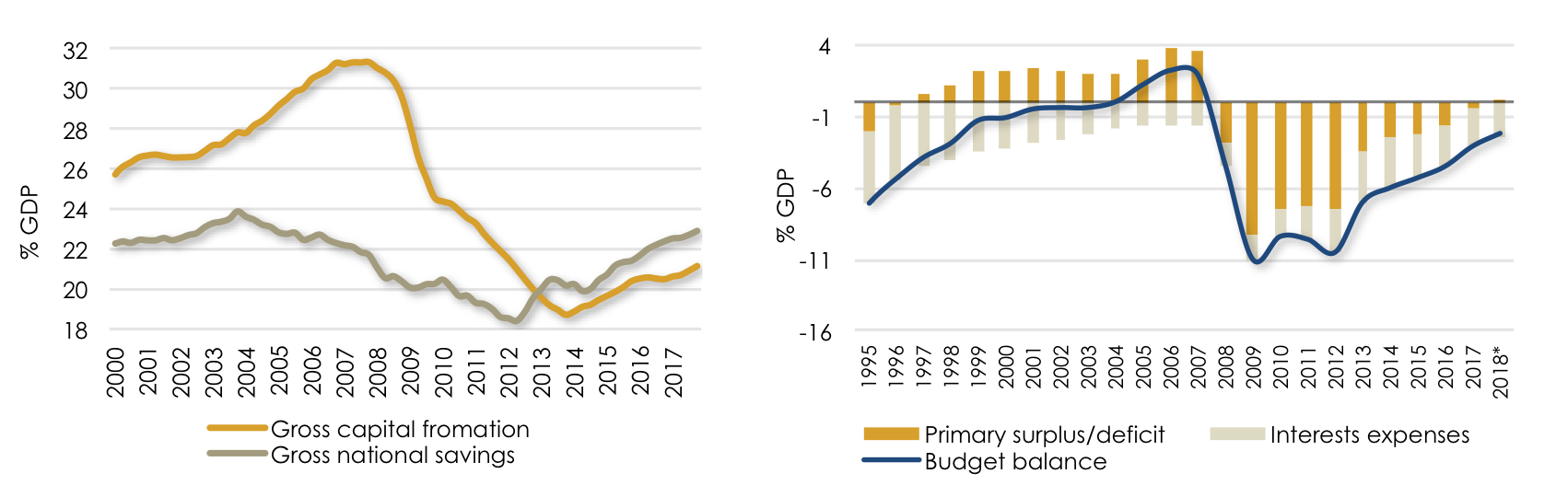

The Spanish economy is progressing with a more solid basis than previous periods of growth; this is revealed, for example, by its current financing capacity, compared to the rest of the world; the current account should report a surplus of approximately 1.8% and 1.7% of GDP in 2018 and 2019, respectively. The robust growth will also facilitate exit from the excessive deficit procedure in the framework of the EU, as public deficit will fall to 2.4% of GDP. Unless Spain overshoots on public spending, a fiscal primary surplus of about 0.1% of GDP should be posted in 2018 after ten years of continued primary deficits.

CHART 1. PERFORMANCE OF NATIONAL INVESTMENT AND SAVINGS RATIOS (LEFT) AND PERFORMANCE OF PRIMARY FISCAL BALANCE AND INTEREST PAYMENTS (RIGHT).

Source: Bank of Spain, Spanish Ministry of Finance and Civil Service, Ee.

However, the setup we consider for the Spanish economy is now subject to upside risks, especially politically motivated but also economic risks, both nationally and globally.

Inside Spain, Catalonia has been growing above the Spanish average in the last three years; however, after the events last autumn, this may not be the case any longer. Among other internal economic risks, high long-term unemployment rates and excessive public debt stand out. Future higher interest rates will exacerbate the risk of financial distress for highly indebted sovereign borrowers, to which we can add, given Spanish energy dependence, the increased price of oil.

Moreover, the situation in Catalonia not only has significant economic effects, but also diverts attention away from important issues, having contributed significantly to the brake on reforms the last few quarters. For some important issues, such as pension reform, we have even observed setbacks in the process. Due to the country’s current political situation and balance, including the motion of no confidence tabled in Parliament on Friday (25 May) against the Government, the reversal of major reforms would be one of the most important internal risks. Yet probabilities of extremist political proposals remain low.

Outside Spain, the Trump Administration continues to move forward with its unilateral agenda, causing a significant increase in uncertainty, which is also having a significant impact on oil prices. On the other side of the Atlantic, and almost two years after holding the referendum in favor of Brexit and one year after the United Kingdom activated the protocol to leave the EU by means of article 50 of the Lisbon Treaty, trade and investment flows between Spain and the United Kingdom are already being affected. On the other hand, markets continue to show a bearish mood regarding the constitution of a populist government in Italy, based on a coalition of extreme left and extreme right parties.

In the current context of solid economic growth but risks on the upside, to lengthen the Spanish economic cycle, it is first necessary not to backtrack on the major economic reforms undertaken the past few years and also to draw up additional reforms that enable extending growth in the medium term. However, this must always fall within the scope of necessary institutional stability. The political capacity to implement these reforms will be a determining factor.

José María Romero Vera

Associate Principal

Economic Analysis and International Affairs