Spanish Regional Governments are clearly benefiting from the intense economic growth of the national economy. As a consequence, average regional non-financial revenue grew above non-financial expenditure in 2017 (6.4% vs. 4.6%). This allowed the regions to achieve in 2017 a deficit of -0.3% of GDP, well below the target (-0.6%).

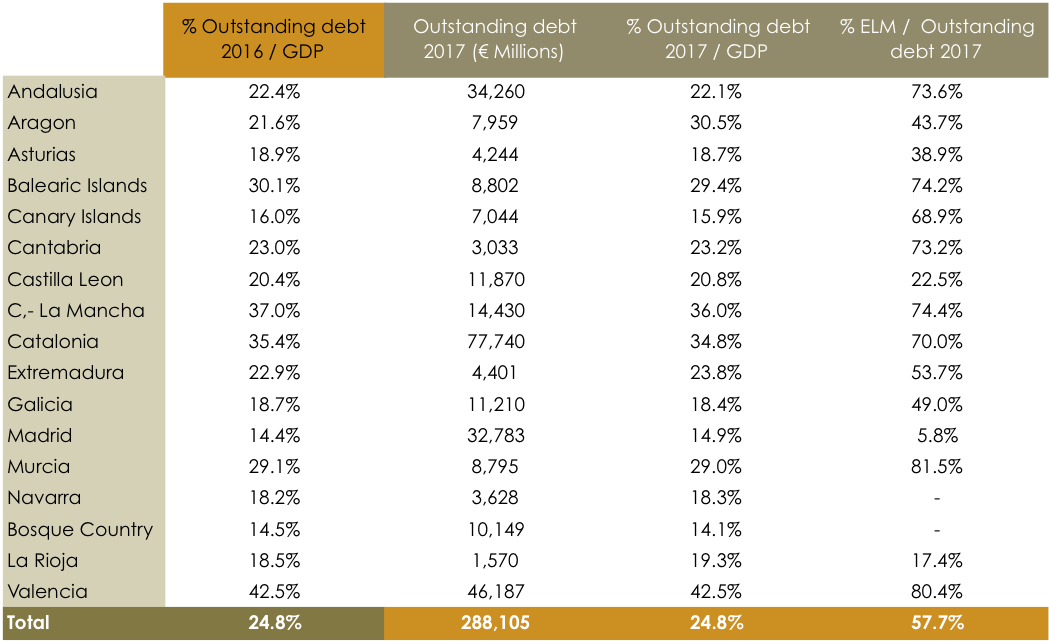

However, there has been a very important increase in the regional debt over the last years. In 2012, outstanding regional debt over GDP ratio was 11%. In five years this ratio has increased up to 24.8% at the end of 2017. Valencia recorded the highest ratio, 42.5%, followed by Castilla-La Mancha, Catalonia and Aragon, all of them with ratios above 30%. Conversely, Basque Country and Madrid remained below 15% (see Table 1). In this context, the Extraordinary Liquidity Mechanisms (ELM) have gained great importance in the share they represent of the regional debt, from 18.1% of the outstanding regional debt in 2012 to 57.7% in 2017. They were put in place by the National Treasury at the peak of the financial squeeze to confront from 2012 onwards the difficulties for Regional and Local Governments to access the financial markets and to pay their suppliers.

TABLE 1. OUTSTANDING DEBT-TO-GDP RATIO.

Source: Bank of Spain, Ee.

In this sense, the above data show the need to review the regional financing system of Regional Governments, on both the revenue and expenditure side. Its reform is still one of the core political debates in the agenda. One of the main points of the reform would be to make sure that the regions reduce their financial dependence on ELM, so that they return to the markets to finance their debts. Furthermore, last month, the Spanish cabinet finally approved the draft bill for State General Budget for 2018. The Draft Bill includes a potential mechanism (“Disposición adicional 136”) to allow negotiations between the Treasury and the Regional Governments for the reduction of the debt-to-GDP ratio and of the annual cost of servicing the regional debt.

In summary: 1) the strong economic growth, the increase in the regional non-financial revenues and the reduction of the regional public deficits should help to make regional debt more sustainable; 2) we expect the return of the regions to the markets to finance their debts and the improvement of their debt-to-GDP ratio.

Ricardo Martinez Rico

President & CEO, Equipo Económico.